Guest Blog By: Jeff Devens, Ph.D.

*This is the fourth article in a series by Dr. Jeff Devens. He’s a humble, extremely knowledgeable advocate for overseas investors, with an impressive knowledge about investment fees, US taxes and Roth 401(k) plans for educators overseas. *

Tax Freedom Day is an annual event representing when taxpayers have earned enough money to pay off their taxes for the year. In 2022, this day was July 17th in France, June 13th in Portugal, June 7th in Spain, May 14th in the UK, June 15th in Canada, and April 18th in The United States. When it comes to earnings, it's not what you make, it’s what you keep after taxes that counts.

In the United States, there are TWO tax tables used to calculate taxes, one for EARNED, and one for UNEARNED INCOME.

Earned Income includes salary from teaching, writing a book, tutoring, coaching, speaking at conferences, and self-employment income. To determine taxes on earned income the IRS utilizes a progressive tax system, meaning there are different tax rates for various levels of earned income. Let's say you're a single teacher earning $58,000 per year. How would you be taxed on this income?

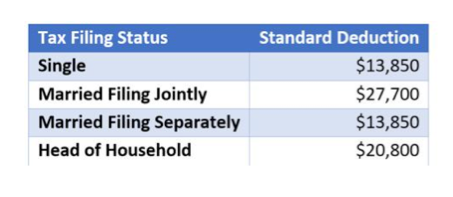

First, we need to subtract the Standard Deduction from total income. This is an amount of money the government allows you to deduct against income before determining taxes. In 2023, this amount for a single filer is $13,850.

$58,000-$13,850 = $44,150. Assuming no additional deductions or tax credits, this figure ($44,150) represents your Adjusted Gross Income (AGI).

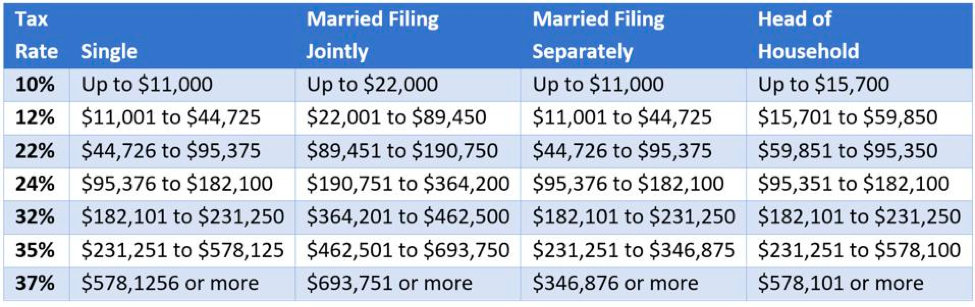

Next, we need to determine how much is owed in federal taxes. Currently, there are seven different tax brackets at the Federal level for earned income. Continuing with our example, with an AGI of $44,150, you would pay 10% on the first $11,000 of this income ($1,100) and 12% on the remaining $33,150 of income ($3,978) for a federal tax ($1,100 + $3,978) = $5,078.

In addition to the federal taxes, we are required to pay Medicare and Social Security Tax (FICA) on earned income. This amount is 6.2% of your total earned income before the standard deduction is applied. 6.2% of $58,000 (income earned before standard deduction) = $3,596.

Federal ($5,078) + FICA ($3,596) = $8,674.

We also need to account for state tax, unless one lives in a state with no state tax. For our example, let's assume you live in Minnesota, a state that utilizes a progressive tax scale similar to federal tax rates. In 2023, the MN state tax rate for an earned income of $44,150 = $2,260.

All total, a single teacher earning $58,000 per year, living in Minnesota, would pay $11,334 in taxes: Federal ($5,078) + FICA ($3,596) + State ($2,660), taking home $46,666.

The good news for international educators is they can avoid paying these various taxes by utilizing the Foreign Earned Income Exclusion (FEIE). We've been able to do this for 27 years and counting. For 2023, the FEIE allows individuals to exclude up to $130,000 of earned income, meaning they would pay no Federal, FICA, or state taxes on earned income below $130,000. If you are married and filing jointly, each of you is eligible for this exclusion. This translates to $260,000 of FEIE exclusions. This is a powerful tax savings tool, both now and in the future.

Unearned Income: What is it, how is it taxed?

Unearned Income is often termed passive income and includes income derived from investments: stocks, bonds, real estate, and dividends. Investments held inside a brokerage account for at least ONE YEAR are taxed at long-term capital gains rates that have preferential tax rates compared to earned income rates. As a result, there are significant tax savings compared to earned income taxation.

Continuing with our single teacher example, let's assume you spent 25 years working abroad, utilizing the FEIE, and invested in index funds inside your brokerage account. Let's assume you invested the same amount each year as you would have paid in taxes had you worked in the United States, $11,334. Assuming an annual 9% return, after 25 years you would have $959,999.95 of unearned income.

Question: How much would you pay in taxes in 2023 if you withdrew $58,000 of UNEARNED income from your brokerage account and had no reported earned income?

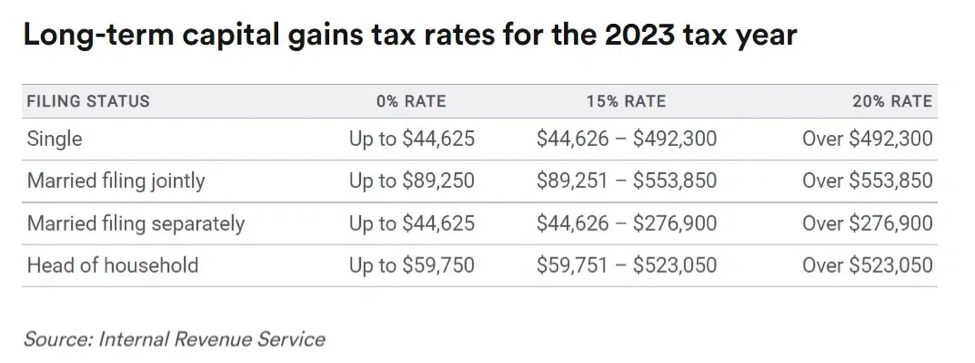

Using the long-term capital gains rates (see below), there is a 0% tax bracket for single filers on the first $44,625 of unearned income. We also have use of the standard deduction ($13,850) to withdraw additional unearned income and pay $0.00 in taxes. Together, $44,625 + $13,850 = $58,425. How much federal and FICA tax would be due? Answer: $0.00. Why? Because unearned income is taxed differently than earned income and does not include taxes for federal or FICA. You will, however, incur a state tax of approximately $2,600. A way to mitigate state taxes would be to move to one of the nine income-tax-free states.

The difference in savings between earned and unearned income for our single teacher is pronounced.

-Earned Income taxes on $58,000 = $11,334

-Unearned income taxes on $58,000 = $2,600

-Difference of $8,734

Over 25 years of retirement, this translates into $218,350 of tax savings. I don't know about you, but that's a lot of cherry cokes and back shavings. Ok, too much information, but you get the point. What could you do with an extra $8,734 in savings each year?

Assuming no earned income, a married couple could withdraw up to $89,250 (0% bracket for LTCG) + $27,700 (MFJ Standard Deduction) = $116,950, in 2023, and pay little to no taxes. It’s important to note, long-term capital gain rates are adjusted for inflation, meaning the rates will increase over the years to account for the declining purchasing power of the dollar.

When I realized the power of brokerage accounts, and how to harvest tax savings, it changed the way I viewed Roth 401K employee plans (often weighed down in fees), Individual Retirement Accounts (IRAs), and Health Savings Accounts (HSAs). For example, unearned income is still counted toward determining Affordable Care Act (ACA) subsidies, Social Security taxation, and eligibility for various tax credits; however, when combined with Roth 401k plans offered by schools and IRA accounts, brokerage accounts can be a POWERFUL tool for generating tax savings and wealth preservation.

In my next blog, I'll provide examples of how to utilize various accounts to offer further tax savings opportunities upon repatriation or retirement.

p.s. Extra credit tax teaser: Assume you have a brokerage account with $959,999.95 and a pre-tax teacher retirement account (i.e.,457,403b,401k) with $250,000. How can you withdraw these pre-tax funds without paying taxes or how could you convert them to a Roth IRA without paying taxes?

Answer: you can withdraw or convert up to your standard deduction (single, $13,850; Married, $27,700, in 2023). If you draw the additional income needed to live from your brokerage account and stay in the 0% tax bracket you would pay little to no taxes. For example, If a married couple required $80,000 per year in retirement, they still have $9,250 of their 0% LTCG tax bracket AND their standard deduction ($27,700) for a total of $36,950. They could use this remaining amount to convert those funds from pre-tax to never-tax, or for stepping up the basis of funds inside their brokerage account. I’ll explain more about how to do this in my next blog.

For the past 27 years, Jeff has served as an international school psychologist, counselor, and educator. In partnership with Human Resources, finance, and the schools Working on Wellness Committee, Jeff provides workshops addressing a myriad of financial topics, with a specific interest in understanding taxation mitigation strategies for Americans. You can reach him at jeffdevens4@gmail.com